How to use the 50/30/20 rule to organize debt payment

Anúncios

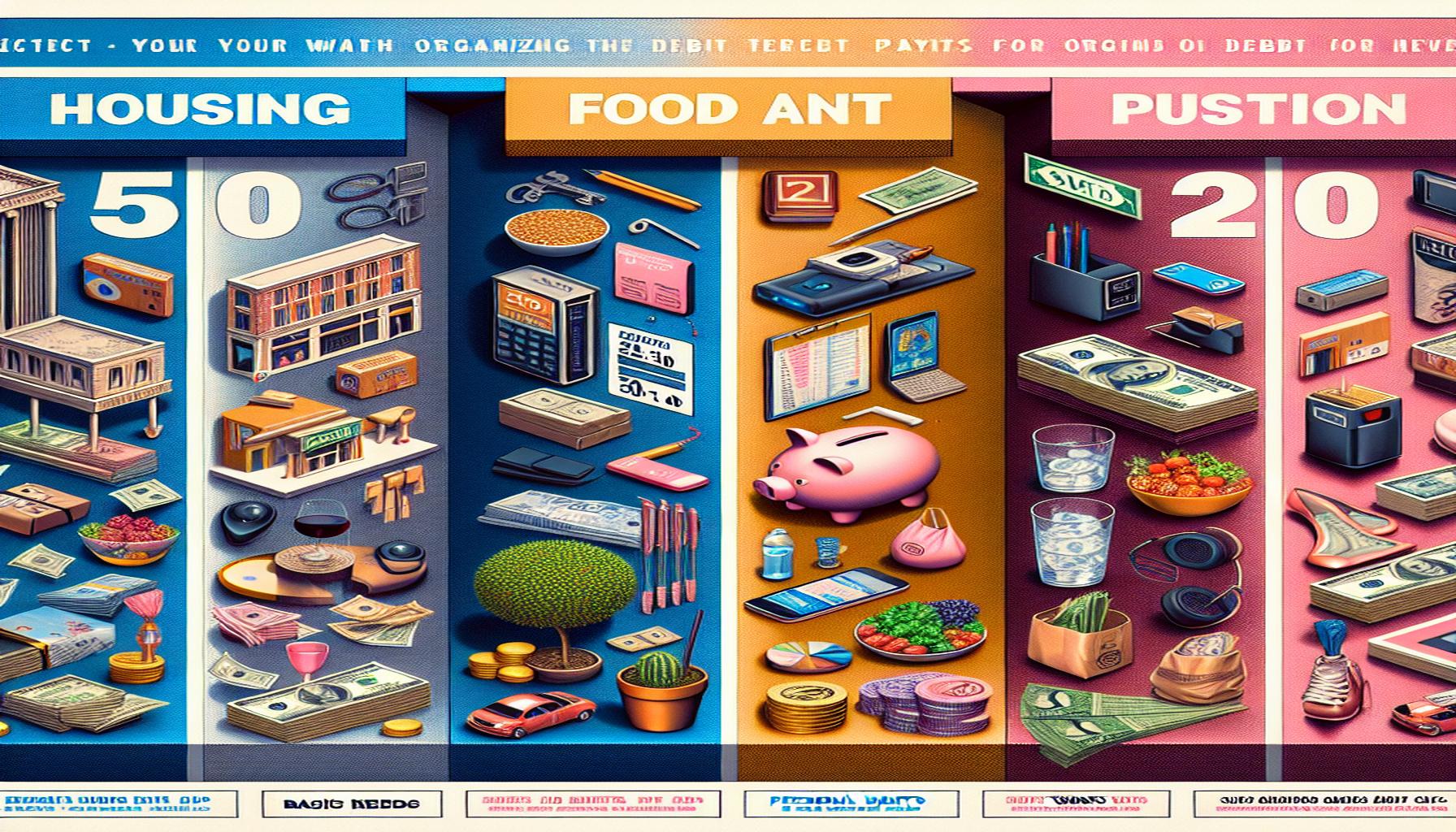

Understanding the 50/30/20 Rule

Managing debt can feel overwhelming, but understanding the right approach can simplify the process. One effective strategy is the 50/30/20 rule, a budgeting framework that helps you allocate your income wisely. By following this guideline, you can create a sustainable financial plan that allows you to meet your needs while also preparing for future financial stability.

Anúncios

This rule divides your after-tax income into three key categories:

- 50% for needs: This includes essential expenses such as housing, groceries, healthcare, transportation, and utilities. For example, your rent or mortgage, food purchases, and necessary bills fall into this category.

- 30% for wants: This category covers non-essential expenses like dining out, entertainment (such as movies and concerts), travel, and hobbies. While these are enjoyable, they are not critical for survival.

- 20% for savings and debt repayment: Focus here on building savings for emergencies or future investment and paying off any existing debts, such as credit cards or student loans. This allocation is crucial for financial health because it helps you create a safety net while also reducing outstanding obligations.

To see how this works in practice, let’s consider an example. Imagine you earn $4,000 per month:

Anúncios

- Your needs would amount to $2,000. This could cover your rent, utilities, car payment, and groceries.

- Your wants would be $1,200. This small portion could allow you to enjoy a couple of dinners out, a subscription service, or a weekend trip.

- Your savings and debt repayment would total $800. This allocation could mean saving for an emergency fund while simultaneously making extra payments on high-interest debt.

This straightforward division not only ensures your essential needs are met but also allows you to enjoy life while steadily addressing your financial obligations. But how can you effectively implement the 50/30/20 rule? Here are a few practical steps:

Steps to Apply the Rule

First, track your income and expenses to get a complete picture of your financial situation. You can use budgeting apps, spreadsheets, or even a simple notebook to log everything and identify how much you spend in each category.

Next, adjust your spending where necessary. If you find that your needs exceed 50%, consider ways to reduce costs. This could mean downsizing your living situation or shopping for groceries more strategically.

After that, begin funneling the allocated 20% into savings accounts and debt repayment plans. Aim to create an emergency fund equivalent to three to six months’ worth of expenses as a safety net. Paying off debt, especially high-interest loans like credit cards, should be a priority to free up more of your income in the future.

By applying the 50/30/20 rule, you can create a clear financial framework, take control of your debt payments, and ultimately work towards achieving financial freedom, enabling a lifestyle that includes both security and enjoyment.

SEE ALSO: Click here to read another article

Implementing the 50/30/20 Rule for Debt Management

Applying the 50/30/20 rule effectively requires a clear understanding of your financial landscape. Start by examining your current income and expenditures closely. This initial step creates a foundation for budgeting. Use simple tools like spreadsheets or mobile apps, which can automate the process of logging your financial activity, making it easier to see where your money goes each month.

Once you have a holistic view of your finances, it is essential to categorize your expenses into the three designated areas: needs, wants, and savings/debt repayment. This method not only helps in planning but also encourages accountability. Here’s a breakdown of how to organize these categories:

- Needs: These are the essentials you cannot live without. Identify your fixed necessary expenses like rent or mortgage, utilities, and groceries. A good practice is to list these needs and compare them against your 50% allocation. If needed, analyze where you can cut costs. Perhaps you can switch to a cheaper phone plan or use public transport instead of driving.

- Wants: This category encompasses all the enjoyable things in life. Make a tally of your discretionary expenses like dining out, entertainment, and hobbies. If you discover your spending here exceeds 30%, consider trimming down on non-essential items. For example, you may choose to limit your restaurant visits or subscribe to one streaming service instead of several.

- Savings and Debt Repayment: The final piece of the puzzle is crucial for your long-term well-being. With the 20% designated for savings and debt repayment, you must decide how much to allocate to each. Prioritize payments on high-interest debts, as this strategy minimizes the interest you pay overall. Aim to pay more than the minimum required to make significant progress in reducing your debts.

Understanding how to distribute this 20% effectively can be empowering. For instance, if you are paying off credit card debts with interest rates of 20% or higher, channel a larger portion of this allocation toward paying down those debts initially. Once these are handled, pivot towards building an emergency fund or putting more into retirement savings.

Remember, flexibility is crucial in this process. Your financial situation can vary month to month, so treat your budget as a living document that you can adjust as needed. If you receive a bonus or a little extra cash, consider using a portion of it to pay down debt faster or grow your savings. The key lies in maintaining discipline while being adaptable to your life changes.

CHECK OUT: Click here to explore more

Adjusting Your Budget Over Time

One of the most significant factors in effectively managing your budget under the 50/30/20 rule is the willingness to adapt and reassess your financial priorities as circumstances change. Life events such as a job change, an unexpected medical bill, or even a significant purchase can all impact your income and expenses. Therefore, periodically reviewing your budget not only helps you stay on track but also reinforces your commitment to repaying debt.

Reevaluating Your Spending Categories

It is essential to check in on your spending habits every few months. Start by revisiting your initial needs and wants assessments. Are there any fixed expenses that you could reduce? For example, if you were previously paying for a gym membership you no longer use, consider canceling it and reallocating those funds to your savings or debt repayment. Similarly, if your job situation changes and your income increases, you might want to reevaluate how much you allocate to paying down debt versus growing your savings.

Additionally, remember that life changes come with new needs. If you’ve recently welcomed a child or moved to a new city, recognize that these transitions may necessitate a reallocation within the 50/30/20 framework. By acknowledging these changes and adjusting accordingly, you can maintain a realistic and effective budget.

Utilizing Windfalls Wisely

Unexpected income, such as tax refunds, bonuses, or cash gifts, can provide an excellent opportunity to boost your debt repayment efforts. Rather than spending these windfalls frivolously, consider using a significant portion of them to make one-off payments towards high-interest debts. For example, if your credit card debt is accruing interest at 18%, applying your tax refund directly to that balance can help you reduce the interest over time and shorten the repayment period.

A combination of extra payments and diligent budgeting can lead to substantial progress. You might choose to allocate a portion of your windfall to build your savings as well; a solid emergency fund can prevent you from incurring more debt in the future by covering unexpected expenses.

Seeking Professional Guidance

If you’re feeling overwhelmed by debt, seeking guidance from a financial advisor can offer tailored strategies suited to your situation. Advisors are equipped to analyze your budget, identify spending patterns, and suggest modifications to effectively implement the 50/30/20 rule. They can also explain complex concepts like debt consolidation or negotiation strategies that can ease your financial burden.

Additionally, financial literacy resources available through community workshops or online courses can empower you with knowledge and skills for better budgeting and financial planning. By educating yourself, you can create a more tailored approach to your budget that considers not just current debts but future financial goals as well.

Incorporating the 50/30/20 rule into your debt repayment strategy is not a one-size-fits-all solution. Be prepared to experiment with different allocations and adjustments throughout your financial journey. Taking ownership of your financial landscape leads to more informed decisions and ultimately grants you greater peace of mind regarding your debt management.

SEE ALSO: Click here to read another article

Final Thoughts on the 50/30/20 Rule for Debt Management

In conclusion, utilizing the 50/30/20 rule can be a powerful method for organizing debt payments while promoting financial stability. By allocating 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment, you’re able to prioritize essential expenses without neglecting the importance of managing debt effectively.

As life’s unpredictability can impact your financial landscape, it is essential to revisit and adjust your budget regularly. Pay close attention to your spending patterns, and don’t hesitate to make changes when necessary. For example, if you find yourself with a bit of extra income through a work bonus or inheritance, consider channeling that windfall directly towards outstanding debts rather than indulging in discretionary expenses.

Moreover, educating yourself about financial matters is crucial. Engaging with resources like financial workshops or working with a professional advisor can provide valuable insight and strategies tailored to your unique circumstances. This additional knowledge can boost your confidence and ultimately empower you to navigate the complexities of debt management with ease.

Remember, the journey to becoming debt-free is not a sprint but a marathon. By practicing discipline, staying informed, and utilizing the 50/30/20 framework, you are setting yourself up for a healthier financial future. Approach this process with patience and adaptability, and you will find that managing debt becomes much more manageable over time.

Related posts:

How to Break the Cycle of Debt with Simple Financial Planning

Best Apps for Debt and Personal Finance Management

Is it worth hiring debt relief companies? Pros and cons

How to Reduce Financial Stress Caused by Accumulated Debt

Common mistakes that prevent people from getting out of debt

How to Organize Your Personal Finances Using Free Spreadsheets

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on the our platform. Her goal is to empower readers with practical advice and strategies for financial success.